Business

Bright Simons: Group Nduom’s Court Victory Doesn’t End Ghana Banking ‘Capital War’

Ghana’s Court of Appeal has quashed the Bank of Ghana’s (BoG) 2019 revocation of GN Savings & Loans’ license, handing a significant legal victory to Group Nduom. But renowned policy analyst Bright Simons warns that the ruling may prove hollow unless the embattled financial institution can resolve deep-seated prudential challenges.

The Appeals Court held that the central bank’s decision was “unfair and unreasonable” because it failed to properly account for Government of Ghana indebtedness to GN Savings & Loans, represented by Interim Payment Certificates (IPCs).

The judges ruled that even if the institution was cashflow insolvent, its balance sheet strength — including those receivables — could have generated future liquidity.

However, Simons, in a detailed analysis published recently, argues that the judgment sidestepped critical prudential questions.

While acknowledging the goodwill toward the Nduom family and their entrepreneurial struggles, he noted that BoG’s 2019 revocation notice alleged far more than a disputed receivable problem — including a negative 61% Capital Adequacy Ratio, a severe liquidity crisis, and GH¢761.55 million in problematic related-party placements.

“The judgment, if it becomes precedent, will seriously clip the wings of the Bank of Ghana,” Simons wrote. But he added: “The Judges did not, in my view, demonstrate an adequate grasp of modern prudential supervision.”

The analyst outlined several hurdles ahead, including the need for fresh capitalization, validation of disputed IPCs, resolution of state claims against GN affiliates, and a credible plan to protect depositors. He noted that GN’s affiliate Blackshield/Gold Coast has been part of a SEC bailout process, with billions of cedis already paid to affected investors, raising questions about the true value of GN’s claimed receivables.

“Fans and friends of the Nduom family deserve to bask in the court victory,” Simons concluded. “But the hard work is only now beginning and the choppy waters have yet to recede.”

The Bank of Ghana is expected to restore the license following the ruling, though operational and capitalization challenges remain unresolved.

Below is Bright Simons’ article in full:

Group Nduom has won one battle but the capital war continues

I just finished reading the judgment of the Court of Appeal in the GN Savings & Loans license revocation saga.

(Quite a few people seem confused. The ruling wasn’t about “GN Bank.” There was a prior downgrade to the Savings & Loans category done with the consent of GN Bank’s directors before the license revocation.)

Quick overview of the judgment

Reading the judgment, I kept smiling because it reinforces my long-held view that policy literacy requires multidisciplinary fluency. No way that judgment can be made sense of in anyway without some basic familiarity and willingness to engage with law, banking, public finance, financial regulation, accounting, auditing, risk management, etc. etc. And, of course, political economy. But this reality seems lost on quite a few people who believe that somehow the complex policy issues facing society can be addressed through siloed commentary. Anyways.

The judgment is well argued, at least judicially. But I think their Lordships retreated to their comfort zone and made the whole issue about “fairness and reasonableness” constitutional tests when quite a big part of the dispute relates to PRUDENTIAL REGULATION.

The judgment, if it becomes precedent, will thus seriously clip the wings of the Bank of Ghana. I doubt that this was the intention of their Lordships. Let’s go over the core findings and issues.

The Appeal Court held that the Bank of Ghana’s (BoG’s) 2019 decision to revoke GN Savings & Loans (S&L) licence on the grounds of insolvency was unfair and unreasonable because, in the court’s view, BoG did not properly account for Government of Ghana / MDA indebtedness to GN S&L. This “indebtedness”, represented by Interim Payment Certificates, should, in their Lordships’ view, have been regarded as receivables assigned to GN S&L, and therefore part of their “asset base”. Properly accounted for, GN S&L’s assets would have exceeded their liabilities. Hence, even if they were cashflow insolvent, they may have still been balance sheet solvent.

The Judges immediately recognised that this holding needed fortification. Because according to the Bank of Ghana Law (Act 930), one can revoke a financial institution’s license EITHER because they are balance sheet insolvent OR because they are cashflow insolvent. There is no dispute that GN S&L were struggling to pay customers and thus were cashflow insolvent.

The Judges dealt with the issue by introducing a caveat into the law. Even if a financial institution is cashflow insolvent but its balance sheet strength could generate liquidity down the line, then the central bank would be unreasonable to declare it insolvent and revoke the license. In short, temporary liquidity problems do not amount to insolvency.

Those of us in public policy would immediately recognise the parallel with IMF debt sustainability analysis. Ghana was asked to restructure its debts because the IMF ruled that the country’s problems were insolvency-related rather than due to mere temporary liquidity challenges.

The issue here is that there are very elaborate technical tests for determining what is temporary illiquidity versus structural insolvency. The Court naturally shied away from that analysis simply by arguing that the Bank of Ghana failed to place any analysis about asset valuation, impairment policies, and long-term liquidity measures before it. Effectively, they were blaming lawyers of the central bank for doing a shoddy job in their representations before the Court.

Without a judicial test to guide the regulator in future, it would be interesting to see how it determines when seemingly impaired balance sheet items can still be regarded as good enough to address liquidity constraints, and over what period or horizon. What is “short-term” in this regard exactly?

Another pillar of the court’s reasoning relates to the essence of the “burden of proof.” The High Court, whose decision GN S&L was appealing, had effectively required the Group Nduom to prove GN was solvent. The Court of Appeal said BoG was the party claiming it was insolvent, and so they should be the ones required to justify their claim.

As far as the Appeal Court was concerned, the High Court should have given real weight to the claimed Government/MDA debts that GN says its affiliate Gold Coast Advisors (GCA) had assigned to it. The ultimate debtors – COCOBOD, Road Fund, GETFund, and ministries, etc. – were all treated as government entities. At this point, the Court makes the argument in passing that lending to the government should be regarded as safe conduct.

Next, the Appeal Court relied heavily on the BoG-appointed supervisor/advisor’s report. Before the license revocation, BoG had appointed an expert to supervise GN’s operations. The final report of the expert was before the Court. In the Judges’ view, the report demonstrated that the supervisor did not recommend immediate revocation and instead recommended remedial measures: removing or restricting Dr Nduom, restricting affiliate transactions, improving ICT/legal systems, branch rationalisation, training, software changes, and assisting GN to recover IPC proceeds.

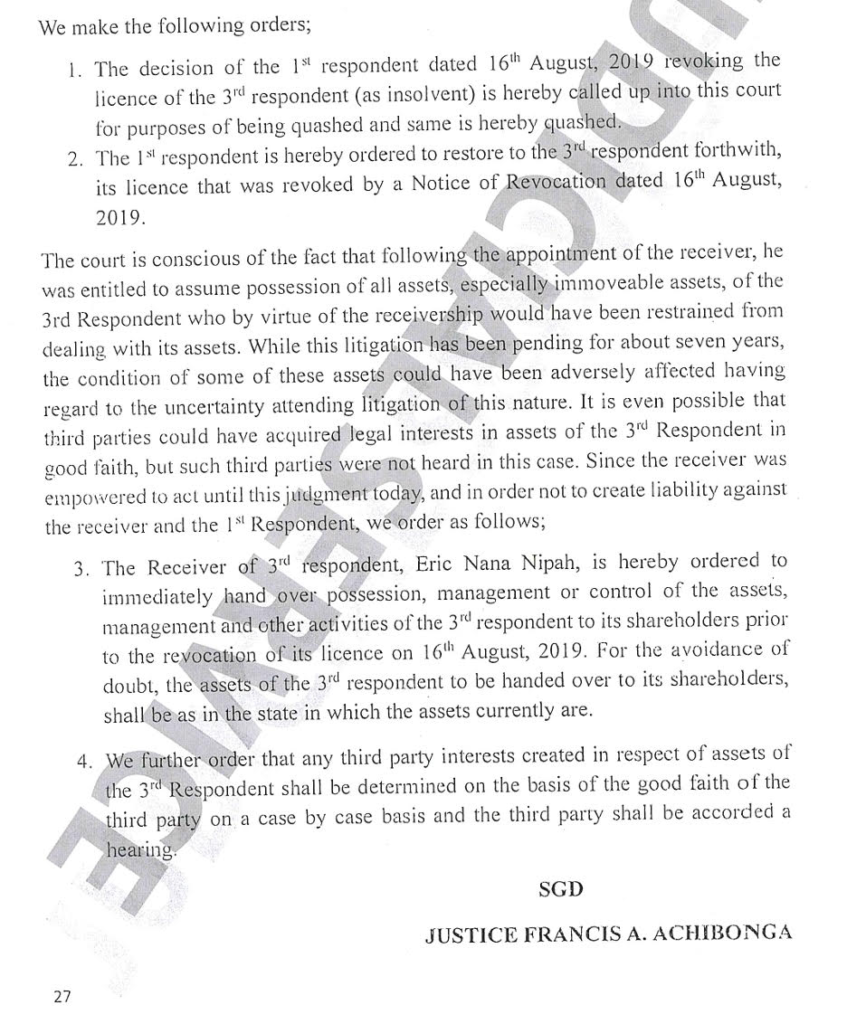

On the back of the analysis, the Court made the following sweeping orders: the revocation decision is quashed; BoG is ordered to restore the licence; the receiver is ordered to hand over possession, management, control of assets and activities to the pre-revocation shareholders; assets are to be handed over “in their current state”; and third-party interests created during receivership are to be handled case by case with hearings.

Issues Arising

Because the Court stayed firmly in the “administrative decision-making reasonableness” domain (what lawyers sometimes call “Wednesbury unreasonableness”), the judgment is understandable as a reaction to a perceived administrative defect: BoG allegedly had evidence from its own supervisor that pointed to remedial action rather than immediate revocation, and yet revoked without sufficiently engaging the IPC/receivables issue. BoG had information about assets that could be used to cure the liquidity constraint, but still chose not to take them into account. Etc.

Still, I am not too sure that the Court’s decision not to wade into the bank-resolution analysis on prudential grounds led to a full and safe disposition of the issues. The judgment feels thin.

BoG’s 2019 revocation notice alleged much more than a disputed receivable problem. It said GN had a Capital Adequacy Ratio of about negative 61%, a severe liquidity crisis, numerous depositor complaints, failure to meet the 10% cash reserve requirement since Q1 2019, failure by shareholders to restore capital/liquidity, and only GH¢30.33m of IPCs confirmed by the Ministry of Finance, which BoG said still did not address a claimed GH¢683.66m capital deficit. The Court very hurriedly skimmed the regulator’s findings, pointed to claims of indebtedness made by GN exceeding the amount of the deficit and then pronounced balance sheet solvency.

BoG also alleged that the insolvency was largely caused by related-party placements/facilities to Groupe Nduom entities, including GH¢761.55m placed with Ghana Growth Fund / Gold Coast Advisors and Gold Coast Fund Management / Blackshield; that some of those funds were used to repay investment-company customers or finance contractors; and that the IPCs were not direct GN-to-Government transactions.

The regulator’s assertions raise serious prudential issues that the Court should have treated with more seriousness because they go to the heart of whether the assets GN claims it has are, enforceable, owned by GN, timely collectible, unencumbered, and valued after impairment.

Under Act 930, banks must maintain policies for non-accrual, provisioning and bad-debt treatment for loans and other exposures. Thus, the IPCs the Court chose to recognise would need to go through “risk adjustment” to ascertain their real value.

The problem, as the Court itself acknowledged, is that these IPCs are the subject of ongoing dispute, seven years on. It is still not clear how much the government of Ghana admits to owing; whether, in light of GN’s other conflicts with third parties, they could have been converted to cash in GN’s favour; and whether the timeline of any conversion would have been realistic under the conditions of commercial deposit-taking banking.

The global accounting standards raise similar issues. IFRS 9 requires expected-credit-loss analysis based on probability-weighted cash-flow expectations, and not hope of eventual collection. IFRS 13 fair-value logic also requires market-participant assumptions, credit risk, timing, and valuation uncertainty. Fair value goes beyond mere invoice face value.

On BoG’s version, the IPCs did not provide assurance since only GH¢30.33m was confirmed by the Ministry of Finance, while the alleged capital deficit was far larger. The Court rejected BoG’s treatment of the evidence, but it did not itself perform a valuation in the prudential sense before deciding to give full weight to GN’s claims.

The Court’s reasoning may throw a wrench into prudential regulation

Where the Court’s judgment introduces some rather hairy concerns is the treatment of liquidity realisation timelines in a banking safety and soundness context.

Banks are confidence institutions. Their core liability – deposits – is often payable on demand or short notice. If a bank cannot pay depositors, the fact that it may hold long-dated, disputed, illiquid receivables is rarely enough assurance. In bank resolution, liquidity failure can itself become solvency failure because asset fire sales, depositor runs, reputational collapse, and regulatory sanctions destroy franchise value, necessitating early intervention. This is the central equation in prudential regulation that seemed to have completely escaped Their Lordships.

The Financial Stability Board’s Key Attributes say resolution should be initiated when a firm is no longer viable or likely no longer viable, with no reasonable prospect of recovery, and that entry should occur before balance-sheet insolvency and before equity is fully wiped out. The BIS summary says something similar.

One cannot fault the Court for privileging administrative fairness, however. They understood that a regulator cannot ignore relevant evidence. They made it clear that BoG should have treated its own advisor/supervisor’s report with more seriousness. I am a long-term critic of the Ghanaian central bank. As I read the judgment, I found myself wistfully remembering many of my clashes with the BoG. A central bank should be much more clinical than the Ghanaian version is wont to be.

But the Judges did not, in my view, demonstrate an adequate grasp of modern prudential supervision.

Modern safety-and-soundness supervision ask questions such as:

-Is capital real, loss-absorbing, and immediately available?

-Are related-party exposures within limits and independently underwritten (BoG flagged GN’s persistent breach of single obligor limits, which itself can be a source of serious asset impairment)?

-Are assets properly classified and provisioned?

-Are liabilities payable on demand being met?

-Is governance fit and proper?

-Can the institution produce reliable accounts?

-Are liquidity ratios being met?

-Is there a credible capital restoration plan?

-Are depositors and financial stability at risk?

Act 930 gives BoG broad powers to set capital methodology, define eligible capital, prescribe capital buffers, impose additional capital for concentration risk, prescribe liquidity requirements, and impose remedial measures. If a Court intends to override that technical judgment, it has no option than to dig into the details. The judgment unfortunately skates the corners.

What now? The Devil is in the Detail

I have a lot of empathy for the Nduom family and Groupe Nduom. Their entrepreneurial travails have been legend. It is so damn hard to build any entrepreneurial edifice of consequence in Africa that one naturally feels a spiritual bond to those trying.

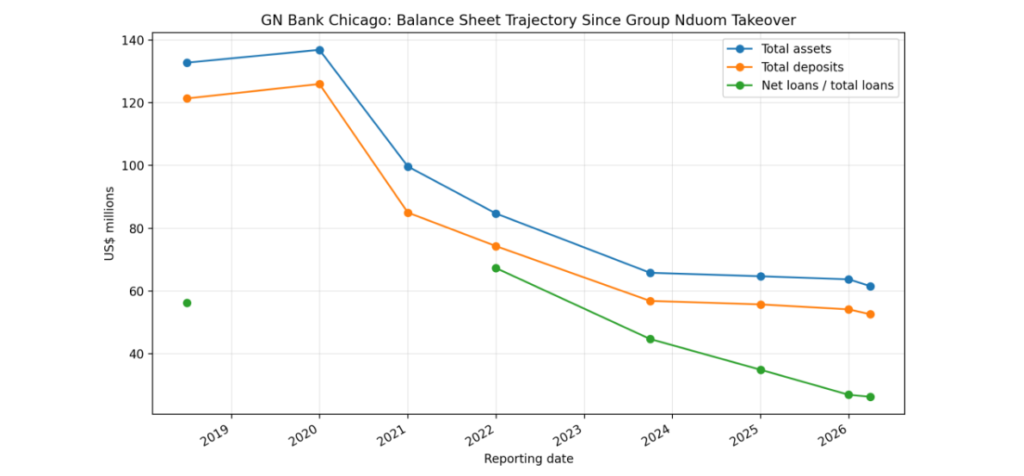

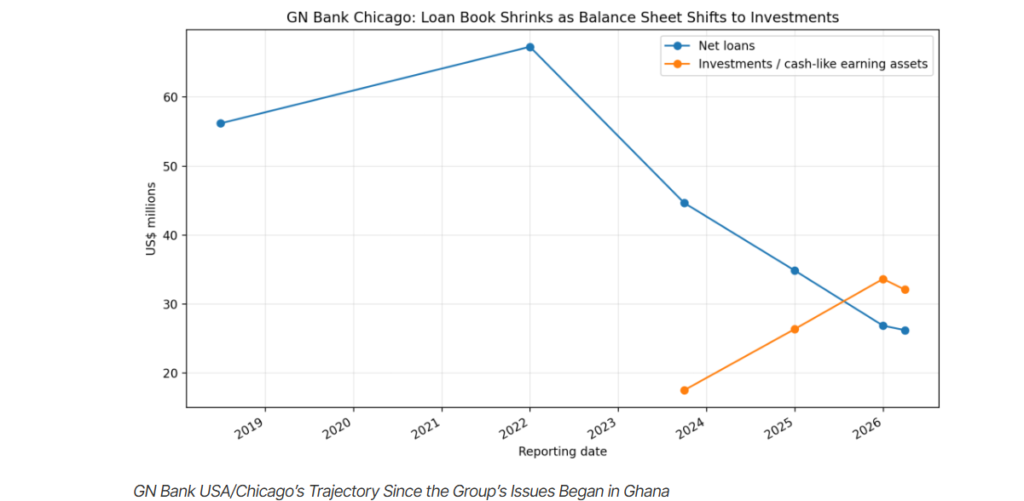

In the midst of GN’s issues in Ghana, GN Bank USA, based in Chicago, also started to face serious challenges leading to regulatory restrictions in 2020 that were only lifted in 2025. The already small bank has now shrunk to a third of its size since 2018. Group Nduom has suffered!

GN Bank USA/Chicago’s Trajectory Since the Group’s Issues Began in Ghana

For that reason alone, there is substantial goodwill. Quite a number of people would like to see the GN brand restored. Even the angry litigants still chasing their money from GN may see glimpses of hope in a restored GN S&L.

But I fear that the road ahead could be bumpy.

Prudential issues remain

The BoG is likely to restore the GN license without further appeals because of the clear political position of the ruling party, which has been to dismiss the prudential issues raised by the previous BoG administration.

But operationally, BoG may worry about whether it can safely allow immediate deposit-taking without a fresh supervisory assessment. GN meanwhile would need a massive deposit mobilisation drive to have the slightest chance of operational success.

Yet, if BoG simply lets GN reopen counters and starts taking deposits, some may argue that it is taking enormous depositor-protection/insurance risk.

Assets “in their current state”

The Judges avoided massive liability risk for the government by ordering that GN’s assets should be returned in their “current state.” This phrase avoids making GN’s receiver liable for all deterioration, but it creates a swamp.

The receiver may have collected loans, sold assets, paid depositors, terminated leases, retrenched staff, transferred records, defended claims, repudiated contracts, paid taxes, and incurred professional fees. Some third parties may have bought assets from the receiver in good faith. Some loans may have been written down or settled. Some depositors may have been paid by the state or through bailout/resolution mechanisms.

Every one of those events creates a massive reconciliation problem.

Depositors and state subrogation

If customers were paid by the state, receiver, deposit-protection scheme, or bailout vehicle, those payments do not vanish. The paying entity may become subrogated to the customers’ claims. That means GN’s liability stack today may include Government or resolution-vehicle claims, not only original retail depositor claims. In patching up the balance sheet, it may emerge that liabilities now far exceeds assets, especially if the IPCs being relied upon end up heavily impaired following recent auditor general evaluations.

The Security & Exchange Commission’s (SEC’s) updates on key affiliates of GN such as Blackshield/Gold Coast are relevant here by analogy and possibly substantively because Gold Coast/Blackshield was part of the same receivable/affiliate story.

SEC has said in the recent past that Blackshield/Gold Coast clients received partial bailout payments and that GHS1.34bn had been paid to 73,541 Blackshield/Gold Coast claims, with GHS757.5m fully settling 61,734 claims. In 2024, SEC announced another GHS1.5bn release for affected investors, including Blackshield/Gold Coast and Kron Capital, on top of GHS4.46bn previously released to affected investors.

If the implication is that Gold Coast/Blackshield or Ghana Growth Fund are insolvent or subject to investor/state claims, then GN’s receivables from those entities may be severely impaired after netting off. A claim against an affiliate with massive crystallised liabilities is not equivalent to cash or, for that matter, Tier 1 capital.

Capitalisation

Which boils down to the most critical question of all: fresh capitalisation. Does GN today have:

-positive net worth after impairment;

-sufficient unimpaired paid-up capital;

-adequate risk-based capital ratio;

-adequate liquidity;

-clean audited accounts;

-no disqualifying related-party exposures;

-reliable systems and governance;

-capacity to resume deposit-taking without threatening depositors.

What all GN’s fans are hoping to hear is when the Government will pay validated receivables; if shareholders are in the position to inject fresh capital; how investors are being brought on to recapitalise; and by what process liabilities will be legally restructured. The IPCs story pales in insignificance before the sheer scale of the challenge.

The Bottomline

For independent analysts, the way forward, if GN Bank is to avoid the zombie status of being a licensed bank on paper without operational activity, appears to be the following:

Completion of the IPC validation (possibly with court cases discontinued);

A determination of what Government truly owes and to whom;

A set off or settlement of state/resolution claims;

A clear plan for shareholder recapitalisation;

A ring-fencing of old claims into a specialised resolution vehicle;

And a final reopening of the institution once a new audited balance sheet and liquidity plan has met objective BoG prudential requirements.

Fans and friends of the Nduom family deserve to bask in the court victory. They have suffered for long.

But the hard work is only now beginning and the choppy waters have yet to recede.

Extract from Judgment

Ghana has lost more than US$16.5 billion in potential gross oil revenue over the past six years as crude oil production plummeted by nearly half from its 2019 peak, according to a devastating new report by the prominent Institute for Energy Security (IES).

The analysis, authored by energy experts Smith Prosper Boahene and Prince Lumor, paints a grim picture of a sector in freefall.

Crude oil output crashed from 71.44 million barrels in 2019 to just 37.30 million barrels in 2025, a staggering decline of almost 48 percent. The Energy Commission projects production will fall further to 34.83 million barrels in 2026, extending the downward trajectory into a seventh consecutive year.

The production collapse has delivered a hammer blow to government finances. Total petroleum receipts nosedived by 43.27 percent, from US$1.36 billion in 2024 to US$770.27 million in 2025. The decline was driven by both lower production volumes and a fall in the average realised crude oil price from US$86.12 to US$74.93 per barrel.

The first half of 2025 alone told a harrowing story: crude oil production declined by 26 percent year-on-year to 18.42 million barrels, while petroleum receipts collapsed from US$840 million to US$370 million.

IES described the prolonged downturn as “not a routine cyclical dip” but a structural crisis born of deep-rooted operational and policy failures.

“The decline is not attributable to one shock, but to several structural, operational, and policy failures compounding over an unusually long period,” the report stated.

Using an “illustrative counterfactual” model, IES projected a scenario in which Ghana maintained a modest annual production growth rate of three percent through sustained drilling, new petroleum agreements and improved reservoir management. Under that scenario, cumulative production would have exceeded actual output by approximately 221 million barrels—a missed opportunity that translates directly into the US$16.5 billion revenue hole.

Petroleum revenue contributes about 10 percent of total government income and supports critical public infrastructure and national development programmes. The sustained collapse therefore has far-reaching implications for Ghana’s fiscal stability, affecting everything from road construction to healthcare funding.

The report identified natural depletion of mature oil fields, insufficient replacement reserves and the failure to sign new petroleum agreements since 2018 as the principal causes. Ghana’s oil production remains dangerously concentrated in just three offshore fields—Jubilee, TEN and Sankofa Gye Nyame. Although Jubilee remained the country’s largest producing field in 2025 with 22.2 million barrels, it also recorded the sharpest year-on-year decline of more than 30 percent, partly due to a planned production shutdown between March 26 and April 8.

IES noted that the temporary production increase recorded in 2024 following drilling under the Jubilee South East project demonstrated that targeted investment can slow production decline. The report also clarified that while COVID-19 disruptions worsened the downturn in 2021, the decline had already begun before the pandemic.

“COVID-19 aggravated an already-declining trend rather than starting it,” the report noted.

Financial economist Professor Lord Mensah has attributed the sharp decline in petroleum revenues to inconsistent fiscal and investment policies, urging government to channel available oil revenues into infrastructure development, agriculture and export-led economic diversification.

IES concluded that Ghana’s prolonged decline in oil production requires urgent policy action.

“Ghana’s six consecutive years of crude oil production decline are far more than a cyclical fluctuation. The data show a structural crisis… Reversing it will require new licensing, accelerated investment, improved operational efficiency, strengthened institutional capacity, and diversified revenue management, implemented with the urgency the data clearly demonstrate is overdue,” the report said.

The World Bank has downgraded Ghana’s flagship Energy Sector Recovery Programme (ESRP) to “Unsatisfactory” status.

The World Bank has cited significant delays in implementation caused by financing constraints and new fiscal controls from the Ministry of Finance for the downgrade.

In its latest report dated June 30, 2026, the Bank highlighted how election-related disruptions and procurement restrictions have slowed key reforms aimed at improving the financial health of the country’s electricity sector.

Only one program indicator was fully achieved during the reporting period, with the Electricity Company of Ghana (ECG) publishing its 2025 audited financial statements. Progress on smart metering, customer service improvements, and the promotion of clean cooking solutions (LPG) remains behind target.

The combined financial losses of ECG and the Northern Electricity Distribution Company have continued to rise, reaching approximately $1.5 billion. The World Bank stressed the need for better coordination to accelerate structural reforms in the energy sector

Implications

The downgrade carries significant implications for the country.

Given that the energy sector has long been one of the largest drivers of Ghana’s national debt, this development signals mounting friction in the country’s economic recovery.

The key implications of this downgrade include:

1. Escalating National Debt and Fiscal Strain

- Accumulating Losses: With the combined financial losses of the Electricity Company of Ghana (ECG) and the Northern Electricity Distribution Company (NEDCo) rising to approximately $1.5 billion, the energy sector remains a massive financial black hole.

- Budgetary Pressure: Because these utilities cannot cover their operational costs, the Ministry of Finance is routinely forced to step in with emergency bailouts. This diverts scarce public funds away from critical sectors like healthcare, education, and infrastructure development.

2. Risk to Investor Confidence and Future Financing

- Negative Signaling: A World Bank downgrade acts as a warning flag to international financial institutions, bilateral donors, and private investors. It signals that structural reforms are stalling.

- Credit and Loan Conditions: This “Unsatisfactory” status could complicate or delay the disbursement of future tranches of financial support from the World Bank or make international credit more expensive for Ghana, as it raises the country’s perceived risk profile.

3. Increased Threat of Power Instability (Dumsor)

- Supply Chain Bottlenecks: The report highlights that implementation delays are caused by “financing constraints.” When ECG and independent power producers (IPPs) face severe liquidity crises, they struggle to maintain equipment, purchase fuel, or pay power generators on time.

- This directly increases the risk of operational disruptions, fuel shortages, and a return to erratic power outages (dumsor), which severely impacts businesses and households.

4. Stalled Modernization and Consumer Upgrades

The downgrade explicitly notes that crucial consumer-facing reforms have fallen behind target:

- Smart Metering & Customer Service: Delays in deploying smart meters mean that power theft, commercial losses, and inefficient billing will continue unchecked.

- Clean Cooking Clean Energy Transition: Delays in promoting clean cooking solutions (like LPG) slow down Ghana’s broader environmental and climate goals, keeping vulnerable populations reliant on biomass (wood and charcoal).

5. Exposure of Political and Structural Roadblocks

- Election-Year Friction: The World Bank explicitly pointed to “election-related disruptions and procurement restrictions” as primary bottlenecks. This implies that political cycles and the resulting strict fiscal controls from the Ministry of Finance are actively hampering long-term economic planning.

- Lack of Institutional Alignment: The call for “better coordination” highlights a friction point between utility management (ECG/NEDCo) and state oversight (Ministry of Finance), suggesting that bureaucratic silos are paralyzing necessary reforms.

The Silver Lining

The only silver lining noted was ECG finally publishing its 2025 audited financial statements.

While this satisfies a basic transparency indicator, it essentially only provides a clearer, official look at how deep the financial deficit actually is, rather than solving the underlying structural crisis.

The Ghanaian government has announced ambitious plans to eliminate the country’s heavy dependence on imported tomatoes within the next four months.

Agriculture Minister Eric Opoku made the pledge while updating Parliament’s Select Committee on Assurances, outlining ongoing interventions to boost domestic tomato farming and reduce reliance on supplies from neighboring Burkina Faso.

Mr Opoku explained that the government is investing in irrigation infrastructure, including solar-powered boreholes, to enable year-round cultivation in major production areas.

He noted that President John Dramani Mahama has taken a personal interest in the initiative. While acknowledging that consumers are currently benefiting from lower food prices, the minister admitted many farmers are struggling with falling incomes.

Proposals to cushion farmers with free fertilizer and expand agro-processing are under consideration to ensure long-term sustainability.

Ghana’s Tomato Production Challenge

Tomato production in Ghana suffers from a complex mix of climate vulnerabilities, infrastructure gaps, and value-chain coordination failures.

Despite having fertile land and high consumption, the country remains structurally dependent on external sources, spending hundreds of millions of dollars annually importing fresh tomatoes from Burkina Faso and processed tomato paste from global suppliers.

The primary issues plaguing Ghana’s tomato production include:

- High Seasonality and Lack of Irrigation

The “Seasonal Trap”: The majority of Ghana’s tomato production relies on rain-fed agriculture. This creates a cycle of peak-season gluts followed by severe off-season shortages (typically from January to May).

Underutilized Infrastructure: While Ghana possesses several irrigation dams, a lack of widespread, functioning dry-season irrigation systems prevents farmers from cultivating tomatoes year-round. This allows neighboring Burkina Faso—which has more stable, small-scale irrigation systems—to dominate the market during Ghana’s lean months.

- High Post-Harvest Losses

Between 30% and 50% of the tomatoes harvested in Ghana never reach consumers.

This massive wastage is driven by a lack of cold-chain storage facilities, poor handling practices, and inadequate transport infrastructure to safely move delicate, perishable produce from rural farms to urban markets.

- Market Fragmentation and Trader Dominance

The tomato supply chain is tightly controlled by powerful trader cartels (often referred to as “Market Queens”).

These traders heavily dictate prices and often prefer to buy from Burkina Faso due to better product consistency, reliability, and established logistics networks, leaving local Ghanaian farmers struggling with falling incomes or unsold crops during harvests.

- Failed Processing and Industrialization

Past attempts to stabilize the sector through local processing factories (such as those in Pwalugu, Wenchi, and Nsawam) have repeatedly failed or struggled to stay operational.

These plants face inconsistent year-round raw material supply, high operating costs, and stiff competition from cheap, imported processed tomato paste from Europe and China.

- Agronomic and Climate Pressures

Tomatoes are highly sensitive to climate fluctuations. Ghanaian farmers frequently grapple with high night temperatures (which impair fruit setting), excessive daytime heat, and severe crop diseases like bacterial wilt.

Additionally, limited access to high-quality, climate-resilient seed varieties and the high cost of fertilizers often lead to low and inconsistent crop yields.

Recent Developments

The vulnerability of this system was highlighted in early 2026 when security disruptions and export restrictions in Burkina Faso caused sudden tomato shortages and price spikes in Ghana.

In response, the Ghanaian government and Agriculture Minister Eric Opoku announced an emergency push to eliminate tomato import dependency within four months.

This strategy focuses on heavily investing in solar-powered boreholes for year-round irrigation, distributing free fertilizer to lower production costs, and expanding local agro-processing to handle future gluts.

-

Ghana News2 days ago

Ghana News2 days agoIn a First for Africa, Ghana and US Sign Landmark Patent Deal to Fast-Track Innovation

-

Ghana News1 day ago

Ghana News1 day agoTop 10 Front-Page Headlines from Ghanaian Newspapers Today: Thursday, July 23, 2026

-

Homes & Real Estate2 days ago

Homes & Real Estate2 days agoRelocating in Ghana: The Property Decisions That Can Make or Break Your Fresh Start

-

Ghana News1 day ago

Ghana News1 day agoAfrica Demands a Seat at the Table: Mahama Calls for Reshaping Global Health Governance

-

Festivals & Events2 days ago

Festivals & Events2 days agoWhy Agona Nyakrom and Swedru Come Alive Every August for Akwambo

-

Taste GH2 days ago

Taste GH2 days agoSoft, Satisfying, and Deeply Rooted: Discover the Comfort of Tuo Zaafi

-

Africa Watch24 hours ago

Africa Watch24 hours agoLiberia Seizes Over $300 Million in Record-Breaking Cocaine Bust

-

Reels & Social Media Highlights17 hours ago

Reels & Social Media Highlights17 hours agoGhana’s X-Rated Thursday: BBC Blasted, DJ KA Trends, and Viral Juju Tests Take Over