Business

These are the 17 Reforms in Ghana’s Cocoa Sector Announced by the Minister Yesterday

Yesterday, Thursday, February 12, 2026, Finance Minister Dr. Cassiel Ato Forson stood before the nation and did something unprecedented: he named the rot, itemized the failures, and then—piece by piece—laid out a rescue plan for Ghana’s battered cocoa sector.

With thousands of farmers unpaid since November 2025, 50,000 metric tonnes of cocoa stranded at port, and COCOBOD buried under GH¢5.8 billion in legacy debt, the emergency Cabinet meeting on February 11 that preceded his press conference wasn’t a policy retreat. It was a rescue mission.

Here are the 17 reforms the Minister announced—and what they actually mean for the farmer, the sector, and the future of Ghanaian cocoa.

1. Immediate Payment to All Affected Cocoa Farmers

“Cabinet has accordingly directed the Ghana Cocoa Board to commence immediate payment of all affected cocoa farmers.”

No committees. No feasibility studies. No “further consultations.” The directive is active. COCOBOD has been ordered to pay—now. Farmers who haven’t seen a cedi since November 2025 are first in line.

2. New COCOBOD Bill to Automate Producer Price Adjustments

The current system allows a CEO to decide what a farmer earns. That ends.

The incoming Cocoa Board Bill will legislate automatic price adjustments tied to three variables: world market price, exchange rate, and other key indicators. No more discretion. No more negotiation. The formula becomes law.

3. 70% Minimum FOB Guarantee—Locked in Legislation

This is the headline. Cabinet has approved a minimum 70% of gross FOB price to be paid to the cocoa farmer.

Not a promise. Not a target. A floor, written into law. When global prices rise, the farmer’s income rises with it—automatically, immediately, and without political intervention.

4. 90% Interim Relief for the Remainder of 2025/2026

Because reforms take time but farmers eat daily, the Producer Price Review Committee met yesterday afternoon ahead of the presser and approved an emergency 90% of achieved gross FOB for the rest of this crop season.

At $4,200 per ton and the prevailing exchange rate, that translates to GH¢41,392 per ton and GH¢2,587 per bag—effective immediately.

5. A New Financing Model: Cocoa Bonds, Not Syndicated Loans

The 32-year-old syndicated loan model is dead. In its place: domestic cocoa bonds.

COCOBOD will issue bonds to raise a revolving fund for cocoa purchases, repayable within each crop year. The goal is independence from buyer financing and the predatory contract terms that came with it.

6. Revival of PBC (Produce Buying Company) as Market Leader

State-owned PBC has been “completely thrown out of business” under the old model. Cabinet has ordered its immediate revival to become the leading Licensed Buying Company in Ghana.

This is not symbolism. This is the state re-entering the buying space to stabilize competition and protect farmers.

7. 50% Minimum Domestic Processing Mandate

Beginning in the 2026/2027 crop season, a minimum of 50% of all cocoa beans must be processed locally.

This will be encoded in the new COCOBOD Bill. No more exporting raw beans while Ghanaian factories sit idle.

8. Immediate Allocation of Remainder Beans to Domestic Processors

For the current crop year, Cabinet has directed that all remaining beans be allocated to local processing companies.

The Minister confirmed that private processors met with him and the Trade Minister yesterday morning and “indicated they have the capacity and willingness to process more than 50% of Ghana’s cocoa beans going forward.”

9. Revival of CPC (Cocoa Processing Company) as Lead Processor

CPC will be revamped as a matter of priority to become Ghana’s flagship cocoa processor.

The Minister did not put a price tag on the revamp, stating operational details will be announced by CPC’s board and management. But the directive is clear: CPC will no longer be an afterthought.

10. GH¢5.8 Billion Legacy Debt Conversion to Ministry of Finance and Bank of Ghana

COCOBOD currently owes:

- GH¢3.7 billion to the Ministry of Finance

- GH¢1.38 billion to the Bank of Ghana

Cabinet has directed that this GH¢5.8 billion be converted onto the books of MoF and BoG to restore COCOBOD’s positive equity and strengthen its balance sheet for the new financing model.

11. GH¢4.35 Billion Road Debt Transferred to Ministries

Between 2014 and 2024, COCOBOD awarded GH¢26.5 billion in road contracts—GH¢21.5 billion between 2018 and 2021 alone.

After a rationalization exercise supervised by the Ministry of Finance and Ministry of Roads, the exposure has been reduced from GH¢21.7 billion to GH¢4.35 billion. Cabinet has directed that this remaining liability be transferred to the Ministry of Roads and Ministry of Finance for payment.

12. COCOBOD Banned from Quasi-Fiscal Expenditures—With Punishments

This is a line-item revolution.

The new Cocoa Board Bill will prohibit COCOBOD from road construction and other non-core expenditures entirely. And here’s the kicker: it will come with punishment if they ever do so.

No more using cocoa money to build roads. No more “special requests.” The board’s job is cocoa. Nothing else.

13. $500 Million World Bank Facility for Cocoa Roads

Announced in the 2026 budget, this facility will take over the construction of cocoa roads entirely.

Roads will still be built. Farmers will still access their farms. But COCOBOD will no longer finance them, and the Ministry of Roads will be accountable for delivery.

14. Concurrent Forensic Audit and Criminal Investigation

Cabinet has directed the Attorney General to commission concurrent forensic audit and criminal investigation into COCOBOD’s activities over the last 8 years.

Not an internal review. Not a “special audit” filed away in a drawer. A criminal investigation, running parallel to financial forensics, with the full weight of the Office of the Attorney General.

15. Immediate Operational Reforms and Cost-Cutting

“Wasteful and uncontrolled expenditure practices are to be curbed immediately.”

Cabinet has directed the Ministry of Finance to initiate immediate reforms at COCOBOD to streamline operations and cut costs. No specific figures were attached, but the directive is unambiguous: the era of unchecked spending ends now.

16. Jute Sacks Mismanagement Referred for Investigation

Responding to a journalist’s question about 18 containers of cocoa jute sacks stranded at port and a fresh $48 million letter of credit opened for unclaimed sacks, the Minister confirmed the matter is part of the Attorney General’s investigation.

“For five years in a row, all the previous administration did was buy jute sacks, not clear them, and order a new set,” Forson said. “It was more or less a procurement agenda, not buying to bag cocoa.”

17. New Producer Price Announced: GH¢41,392/Ton

Effective Thursday, February 12, 2026, the producer price for the remainder of the 2025/2026 crop season is:

- GH¢41,392 per metric ton

- GH¢2,587 per bag of 64kg

This represents 90% of the achieved gross FOB of $4,200 per ton—a deliberate cushion against the global price collapse while maintaining sector sustainability.

“Never Again”: A New Era?

At least four times during the press conference, the Minister returned to the same phrase: “Never again.”

Never again will a CEO have the power to cheat the farmer. Never again will a board chair determine who gets paid and who doesn’t. Never again will cocoa money build roads while farmers cannot afford school fees.

“Unfortunately, in the past, when the world market price moved up, the cocoa farmer did not benefit,” Forson said. “When the exchange rate depreciated, the cocoa farmer did not benefit. Never again should this practice be allowed to persist.”

The reforms announced yesterday are not merely administrative. They are structural. They are legislative. And if implemented, they will fundamentally rewire who cocoa works for in Ghana.

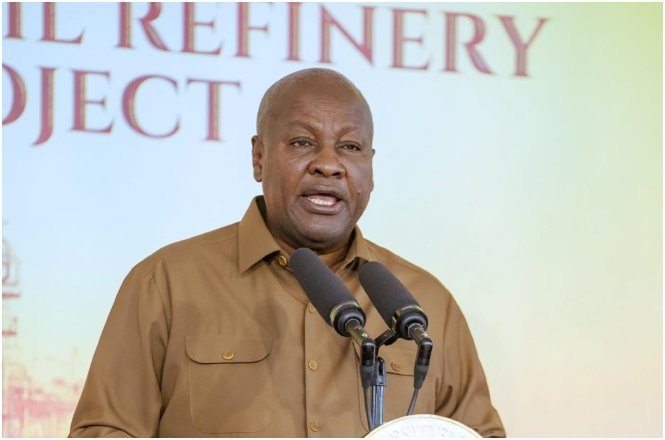

President John Dramani Mahama recently cut the sod for Phase II of the Sentuo Oil Refinery Expansion Project. This US$1.2 billion investment will raise Ghana’s refining capacity from 40,000 to 100,000 barrels per day. The ceremony was more than a groundbreaking event – it was a declaration that Ghana’s energy sector is open for business and that the diaspora is invited.

Here is why Ghana’s energy sector represents one of the most compelling investment opportunities for the global Ghanaian diaspora right now.

1. Macroeconomic stability has returned – and it’s real

When President Mahama assumed office in January 2025, Ghana’s economy was emerging from one of its most difficult periods. Inflation had peaked at 23.8 per cent, the currency was volatile, and investor confidence was weakened.

Eighteen months later, the picture is dramatically different.

| Indicator | December 2024 | April 2026 |

|---|---|---|

| Inflation | 23.8% | 3.4% |

| International Reserves | US$8.9 billion | US$13.8 billion |

| GDP Growth | – | ~6% in 2025 |

| GDP | – | US$114 billion |

Inflation has collapsed from 23.8 per cent to 3.4 per cent. International reserves have strengthened from approximately US$8.9 billion to nearly US$13.8 billion. The Ghana cedi has stabilised and appreciated against major international currencies. Ghana’s economy expanded by approximately 6 per cent in 2025, with GDP crossing US$114 billion, making Ghana one of Africa’s leading economies.

Ghana’s Ambassador to the United States, Victor Emmanuel Smith, has described political stability, credibility, and predictability as the country’s “most powerful tools for attracting global investment”. As one investor at the Economic Dialogue in Atlanta put it:

“Stability is the new alpha. Ghana offers exactly what global capital is now searching for – peaceful rule, democratic governance, and peaceful transitions”.

2. Upstream oil and gas: US$3.5 billion in new commitments

Ghana’s upstream petroleum sector is experiencing a renaissance. Partners in the Jubilee and TEN fields have committed US$2 billion by 2028 to increase oil and gas production, while Sankofa field partners have pledged another US$1.5 billion to boost gas output.

This US$3.5 billion injection is funding new well developments across productive fields and scaling domestic natural gas production from 270 million to 350 million standard cubic feet per day.

President Mahama confirmed that production from the Jubilee field has increased significantly, from approximately 60,000 barrels per day to about 85,000 barrels per day currently. For the first time in several years, Ghana is poised to record an increase in crude oil production, reversing a multi-year decline.

What this means for diaspora investors:

- GNPC is seeking global investors for over 20 new oil and gas exploration fields

- The Voltaian Basin – Ghana’s most significant frontier onshore opportunity – is open for strategic partnerships. GNPC’s exploration subsidiary, ExplorCo, is poised to begin onshore drilling before the end of 2026

- The Accra-Keta Basin offers more than 15 new ocean locations for drilling, ranging from shallow waters to ultra-deep-sea zones

- A new “sliding scale” royalty system adjusts tax cuts dynamically based on production levels and oil prices, ensuring fair terms even when market conditions change.

3. Downstream refining: Sentuo’s expansion changes the game

The Sentuo Oil Refinery expansion is transformative. Upon completion, Ghana’s refining capacity will more than double from 40,000 to 100,000 barrels per day. Employment at the facility will rise from about 800 to 1,500 workers.

But the significance goes far beyond jobs.

President Mahama’s vision is clear:

“Ghana should not be known merely as a producer of crude oil. Ghana should be recognised as a nation that refines, processes, and adds value to its resources, and also become a net exporter of petroleum products”.

When Sentuo completes Phase II and the Tema Oil Refinery is fully operational, Ghana will have more than enough capacity to feed local demand – and export the rest to neighbouring countries.

The government has already demonstrated its commitment to local refining. In a deliberate and strategic decision, one million barrels of crude oil from the Jubilee Field were allocated for refining at Sentuo.

What this means for diaspora investors:

- The Petroleum Hub Project – a US$60 billion integrated energy and petrochemical complex in Jomoro, Western Region – will comprise three refineries with a total capacity of 900,000 barrels per day

- The hub offers opportunities for diaspora investment in refinery development, petrochemical facilities, logistics infrastructure, and energy transition projects.

4. Ghana is positioning itself as West Africa’s energy hub

Ghana’s ambition extends beyond self-sufficiency. The country is positioning itself as the preferred energy and industrial hub for the West African sub-region.

The numbers tell the story. Once Sentuo and Tema Oil Refinery are fully operational, Ghana will have enough capacity to export refined petroleum products to neighbouring countries – strengthening the cedi, improving the balance of payments, and deepening industrial capacity.

Energy Minister John Abdulai Jinapor has confirmed that the government has “reversed the power deficit situation, declining oil production and the weakened investor confidence” through the Reset Agenda. The energy sector is now experiencing renewed growth and stability.

5. Local content: A deliberate invitation to diaspora businesses

President Mahama has been explicit: local content “must be viewed not merely as a regulatory obligation, but as a critical pillar of our national development strategy”.

The government expects “meaningful participation by Ghanaian companies throughout the value chain” and “deliberate investment in skills development”.

Dr Tony Aubynn, CEO of the Petroleum Hub Development Corporation, has called for a “bold and forward-looking economic partnership between Ghana and its diaspora community”. His message to diasporans is clear:

“The Petroleum Hub is a game-changing national asset, and we need our diaspora as co-investors, innovators, and partners in expanding Ghana’s energy economy”.

What this means for diaspora investors:

- Diaspora bonds for energy and industrial infrastructure, offering competitive returns backed by transparent governance

- Co-investment frameworks enabling diaspora investors to partner with institutional investors, private equity funds, and state-backed entities

- Financing local startups and SME supply chains in logistics, maintenance, fabrication, technology solutions, and energy services

- The diaspora can play a catalytic role in financing Ghana’s next generation of energy and industrial startups.

6. Investment incentives are attractive and transparent

Ghana has created a compelling incentive framework for investors, including:

- 10-year corporate tax holiday for qualifying enterprises

- Exemptions from import duties on qualifying equipment and inputs

- Unrestricted repatriation of profits and dividends

- No minimum capital requirement for companies owned by Ghanaians (including those in the diaspora)

- A “one-stop-shop” system for permits, giving investors a single, fast-track approval process with a strict deadline

The Ghana Investment Promotion Centre (GIPC) has stressed the need for “diaspora capital to be channelled into transparent and well-governed investment structures”. Ghana maintained its 6th position on the African continent to invest in 2025 and 2026, according to Rand Merchant Bank.

7. The 24-Hour Economy and Accelerated Export Development Programme

President Mahama’s flagship 24-Hour Economy initiative is designed to maximise the utilisation of infrastructure, industry, labour, logistics, ports, and energy systems around the clock. It presents enormous opportunities for investors in logistics, industrial parks, warehousing, cold-chain systems, transport, agro-processing, manufacturing, retail, ICT, and energy.

The program is aligned with the Accelerated Export Development Programme and the government’s vision of building “a productive, export-oriented, industrialised and technology-driven economy that creates opportunities for our people and competitive returns for investors”.

8. How to get started

For diaspora investors ready to engage, here is a practical roadmap:

| Step | Action |

|---|---|

| 1 | Register with the Ghana Investment Promotion Centre (GIPC) – enterprises with foreign ownership are required to register before commencing operations |

| 2 | Explore incentives under the Free Zones Scheme, including tax holidays and duty exemptions |

| 3 | Connect with the Petroleum Hub Development Corporation (PHDC) for large-scale energy projects |

| 4 | Explore the GNPC’s investment opportunities in exploration, production, and the Voltaian Basin |

| 5 | Consider diaspora bonds and co-investment frameworks for energy infrastructure |

| 6 | Leverage the “one-stop-shop” permit system for streamlined approvals |

The bottom line

Ghana’s energy sector is not just growing – it is transforming. US$3.5 billion in upstream commitments, a refining capacity poised to double, a US$60 billion Petroleum Hub on the horizon, and a government that has made local content and diaspora engagement central to its industrial strategy.

President Mahama’s words at the Sentuo ground-breaking captured the moment:

“This investment is a powerful vote of confidence in our future and in the vast opportunities that Ghana continues to offer”.

For the global Ghanaian diaspora, that vote of confidence is also an invitation.

In a landmark shift that challenges the dominance of the US dollar in Africa’s commodity trade, Ghana has reached an agreement with its large-scale mining companies to purchase 30 per cent of their gold output in Ghana cedis, effective 1 July 2026.

The agreement, brokered by the Ghana Gold Board (GoldBod) under the joint direction of the Minister of Finance and the Minister for Lands and Natural Resources, marks a decisive break from the previous 2022 arrangement between the Bank of Ghana and the Chamber of Mines. Under that earlier framework, gold was supplied in refined bullion form, often exported before settlement, with pricing based on international spot prices converted using the Bank of Ghana reference rate.

Now, each large-scale mining company will sell 30 per cent of its gold output to GoldBod locally in Ghana, in doré (raw) form, at a discount of 0.55 per cent. All purchases will be conducted in Ghana cedis at the Bank of Ghana Reference Rate.

A strategic de-dollarization move

The policy represents a calculated effort to reduce Ghana’s dependence on foreign currencies in its most valuable export sector. By requiring gold transactions to be settled in cedis, the government is effectively creating domestic demand for the national currency and insulating the gold trade from dollar volatility.

Ghana, Africa’s biggest gold producer, launched its domestic gold purchase program in 2022, when the Bank of Ghana began buying a portion of gold produced by mining companies to diversify the country’s foreign reserves. The program initially required industrial miners to sell 20 per cent of their annual gold output to the central bank, helping Ghana’s gold holdings rise to 19.2 metric tons by February. Earlier this year, the government revamped the initiative with the ambitious goal of increasing reserves to as much as 157 metric tons by 2028.

The shift from dollar-denominated to cedi-denominated gold purchases aligns with a broader African trend. Central banks across the continent are increasingly buying domestic gold to strengthen reserves and reduce dollar dependence. As vital global gold suppliers, African countries are seeking to break away from “outdated colonial-era pricing and trading frameworks” and participate in building a more diversified global monetary architecture.

Strengthening the cedi and building reserves

The new gold purchase agreement forms a key pillar of the Ghana Accelerated National Reserve Accumulation Program (GANRAP), which aims to build foreign reserves equivalent to 15 months of import cover by the end of 2028. The program targets intermediate milestones of 8.6 months by the end of 2026.

GoldBod already purchases the entire output of Ghana’s artisanal and small-scale gold mining sector, and the new agreement extends this mandate to large-scale producers. Increased gold reserves protect the country against external economic shocks and can be sold abroad to generate dollar income when needed.

The policy has already demonstrated its effectiveness. GoldBod’s gold exports contributed to a 41 per cent appreciation of the Ghana cedi against the US dollar in 2025, while foreign reserves grew from approximately $8.98 billion in December 2024 to $13.8 billion by the end of December 2025. The Gold Board expended approximately $16.1 billion on gold purchases between January 2025 and May 2026.

Path to LBMA accreditation and zero raw exports

Beyond currency considerations, the agreement has been strategically designed to help Ghana secure London Bullion Market Association (LBMA) accreditation for at least one domestic gold refinery by 2030. LBMA accreditation is critically important in the global gold industry because it sets the highest standards for gold refiners and ensures that their output is internationally recognized and tradable.

All doré gold bought by GoldBod will be refined locally to maximise value retention within the country. After local refining, the gold will be sent to an LBMA-accredited refinery for melting and stamping before being delivered to the Bank of Ghana as part of the nation’s gold reserves.

The arrangement also aligns with President John Dramani Mahama’s vision of achieving zero raw mineral exports by 2030 through increased local processing and value addition.

Implementation details

The Memorandum of Understanding was signed by the Ministry of Finance, the Ministry of Lands and Natural Resources, the Ghana Gold Board, the Bank of Ghana, and the Ghana Chamber of Mines. Further details of the agreement are expected to be made public on Monday, 29 July 2026.

GoldBod has also announced a new official gold pricing regime effective 1 July 2026, with prices released twice daily at 10:30 a.m. and 3:00 p.m. in line with the LBMA Gold Price AM and PM benchmarks, converted into cedis using the Bank of Ghana Reference Rate.

Business

Ghana’s $5 Billion Export Boom Creates Prime Entry Point for Diaspora-backed Processing Plants – Here’s How

Ghana’s non-traditional export sector has shattered the $5 billion mark for the first time, recording a historic 30.7 per cent surge to $5.006 billion in 2025.

But for diaspora investors watching from abroad, the real story lies not in the headline number, but in what it reveals: a massive, untapped opportunity in agro-processing that could multiply returns while transforming Ghana’s industrial base.

Processed and semi-processed products now account for more than 83 per cent of total non-traditional export earnings, with cocoa derivatives alone — including butter, paste, and powder — contributing over US$3 billion. Yet officials acknowledge that Ghana is still exporting the bulk of its agricultural produce at intermediate stages, leaving billions in potential value on the table for investors willing to build the final processing and packaging infrastructure that commands premium prices in Western supermarkets.

The diaspora opportunity: capturing the “missing middle”

For Ghanaian diaspora investors with capital, global retail networks, and a desire to scale African value chains, the timing could not be more opportune. The government has made diaspora engagement a central pillar of its economic transformation agenda, with the Ghana Investment Promotion Centre (GIPC) establishing a dedicated Diaspora Desk to provide regulatory guidance, aftercare services, and access to verified land through an in-house land bank.

“Value addition in agro-processing, digital financial services, and green construction is gaining traction, driven partly by diaspora-led innovation,” said Kwame Kesse-Agyepong, Head of Investment and Business Development at the GIPC.

He noted that Ghana is already seeing strong interest from diaspora entrepreneurs across manufacturing, fintech, renewable energy, and tourism.

Key commodities driving the export surge — cashew nuts, shea nuts, coconut, yams, mangoes, and processed agricultural products — offer prime entry points for diaspora-backed ventures. Yams alone recorded a sharp 559 per cent increase in exports. Each of these products presents opportunities for investments in drying, milling, refining, cold-chain logistics, quality-certified packaging, and branded finished goods for export to Europe, North America, and Asia.

Policy tailwinds and incentives

The government has rolled out a suite of incentives designed to attract diaspora capital into the real sector:

- A new e-visa system launching in the first quarter of 2026 with reduced fees specifically for the global African diaspora.

- The Accelerated Export Development Program, chaired by President Mahama, targeting US$10 billion in non-traditional export earnings by 2030.

- Ghana’s Free Zones Scheme offering a 10-year corporate tax holiday, exemptions from import duties, and unrestricted repatriation of profits and dividends.

- The Feed the Industry Program, strengthening the link between agriculture and industry by ensuring a steady supply of raw materials for agro-processing.

- Reforms abolishing the US$200,000 minimum capital requirement for joint ventures with Ghanaian participation and the US$500,000 minimum for wholly foreign-owned enterprises.

Additionally, the Bank of Ghana is working with commercial banks to develop investment-linked remittance products aimed at channelling diaspora inflows — which reached a record US$7.8 billion in 2025 — into infrastructure projects and long-term capital formation.

A strategic gateway to Africa

Beyond Ghana’s borders, diaspora investors gain a strategic advantage: access to the African Continental Free Trade Area (AfCFTA), the world’s largest free-trade zone by number of participating countries. Africa now accounts for 30.36 per cent of Ghana’s non-traditional export earnings, largely driven by intra-ECOWAS trade. By establishing processing plants in Ghana, diaspora investors can export value-added goods duty-free to 1.4 billion Africans while also leveraging Ghana’s AGOA benefits for the US market.

The road ahead

GEPA CEO Francis Kojo Kwarteng Arthur has appealed for an increase in the Authority’s share of the import levy from 10 per cent to 20 per cent to accelerate progress toward the US$10 billion target by 2030.

“If 10 per cent can generate over $5 billion in export earnings, then 20 per cent will yield even greater results in foreign exchange generation, job creation and industrial transformation,” he said.

For diaspora investors, the message from Accra is clear: the export boom has created a runway. The question is who will capture the value.

-

Ghana News22 hours ago

Ghana News22 hours agoGhana’s Nationwide Flood Clean-Up Kicks Off with Slow Start

-

Ghana News2 days ago

Ghana News2 days agoTop 10 Newspaper Front Page Headlines Today: Thursday, July 9, 2026

-

Ghana News2 days ago

Ghana News2 days ago75 Bank Staff Dismissed as Fraud Surges, Safo Kantanka Left Huge Portions of His Wealth to Maids, and Other Big Stories in Ghana Today

-

Ghana News2 days ago

Ghana News2 days agoPresident Mahama Backs Tighter Checks on His Own Office in Upcoming Constitution Vote

-

Homes & Real Estate23 hours ago

Homes & Real Estate23 hours agoGhana’s Rising Home Prices: Bubble or the Cost of a Growing Nation?

-

Arts and GH Heritage2 days ago

Arts and GH Heritage2 days agoA Few Drops, Many Generations: The Enduring Meaning of Libation

-

Ghana News23 hours ago

Top 10 Newspaper Front Page Headlines in Ghana Today: Friday, July 10, 2026

-

Reels & Social Media Highlights2 days ago

Reels & Social Media Highlights2 days agoExtradition Drama, Galamsey Threats, and Wholesome Romance Rule the Timeline