Perspectives

Bank of Ghana Balances on a Knife Edge

In this detailed analysis, Bright Simons dissects the Bank of Ghana’s audited 2025 financial statements, revealing that the central bank recorded a net loss of GH¢1.25 billion and a total comprehensive loss of GH¢2.80 billion. These losses have pushed its negative equity to approximately GH¢9 billion. Simons explains that the Bank is caught in a costly cycle, often described as a “sterilization treadmill,” where it mops up excess liquidity by borrowing back printed cedis at high interest rates. This process cost the Bank GH¢1.34 billion in 2025 alone, a figure that exceeds its total operating income.

Bank of Ghana Balances on a Knife Edge

By Bright Simons

Preliminaries

On 30th April, 2026, the Bank of Ghana (BoG) published its audited financial statements for 2025. By law, these should have been approved by the Board and submitted to the Finance Minister by end-March. They were not.

The Bank obtained a one-month extension, partly on the grounds that it had changed auditors – from Deloitte to KPMG – who needed time to come to terms with the books. And partly because additional scrutiny was requested around the gold operations and the Bank’s exposure to the Ghana Gold Board (GoldBod).

The statements were approved on 29 April and published on 1 May, barely meeting the secondary legal deadline for publication.

The numbers dropped like a bombshell into Ghana’s polarised political environment. As it became clear that the BoG recorded a net loss of $1.25 billion for the year, the Opposition NPP began to bay for blood. [The dollar amounts used throughout the text are sensitive to specific exchange rate assumptions, and may differ slightly from those in my earlier social media posts.]

Further reading showed that an additional $1.55 billion in other comprehensive income charges – driven by the accounting impact of a stronger cedi reducing the domestic-currency value of dollar assets of the BoG mostly held abroad – pushed total comprehensive losses to $2.80 billion. Cumulative negative equity (the “hole” in the BoG’s capital base) reached ~$9 billion at the end-2025 closing rate, widening from $3.99 billion a year earlier. As a share of GDP, the negative equity is approximately 8 per cent (depending on how exactly one estimates the relevant GDP metric). It is among the largest such positions reported by any central bank globally, and sustained across successive years. Big deal.

Three forces got us here, each one with its own fascinating story to tell.

Getting down to basics

Before examining the numbers, it helps to understand the basic mechanics of what the central bank does that generates these losses. It is not all that complicated, but it can get confusing pretty quickly.

Step 1: Creating Money to Buy Gold

Ghana produces gold, lots of it. It is Africa’s largest producer in fact. The Bank of Ghana wants this gold because it can be sold for dollars, and dollars are extremely precious in Ghana because they often dry up and drag the Cedi down. So, the Bank pays Cedis to the miners and takes their gold. But it is not like it has an infinite stash of cedis sitting in a vault. It usually “creates” what it needs, almost from thin air. When the Bank credits a GoldBod aggregator’s account for onward payment to miners, those cedis come into existence at that moment.

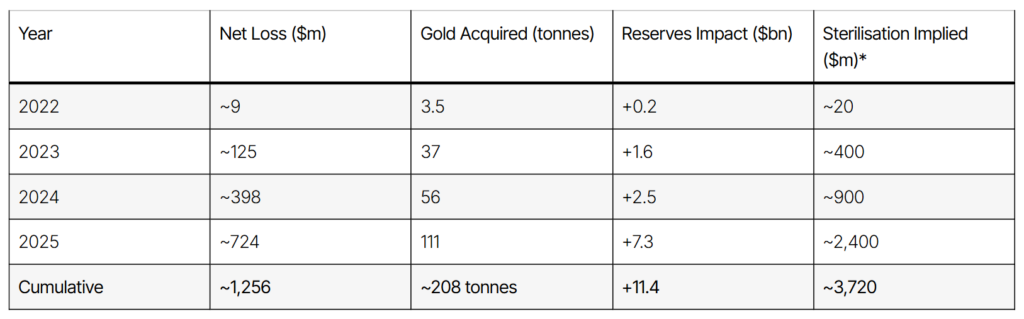

In 2025, the Bank purchased, in one set of transactions, approximately 2.9 million fine ounces of doré gold, worth roughly $7.6 billion at average market prices. Much of the funds used to pay for that gold was created in the way described above.

Step 2: Turning Gold into Dollars

The doré gold is shipped to LBMA-certified refineries, processed into investment-grade “bullion”, and either held as a reserve asset or sold on international markets. In 2025, the Bank sold 869,915 ounces of refined bullion for approximately $3.6 billion, and also sold roughly 2.9 million ounces of doré under the Gold for Reserves programme. The dollars flow into Ghana’s foreign reserves. Result: reserves rose from around $6.5 billion in early 2024 to $13.8 billion by end-2025, a high point in Ghana’s monetary history.

Step 3: Mopping Up the Cedis

But there is a catch, that I have spent months talking about. The cedis created in Step 1 are now circulating in the economy. If left there, banks will lend them, businesses and households will spend them, demand will outstrip supply, and prices of goods will rise. Inflation. The Bank’s primary mandate is to prevent exactly that. So, it needs to pull as much of those cedis back out as possible.

It does this by issuing short-term bills to commercial banks (in simple terms, it borrows from the bank and park the money). A bank hands the Bank of Ghana $8 million worth of cedis; the BoG gives the bank a piece of paper – IOU – promising to pay it back with interest in 14, 28, or 56 days. The cash is locked up. This process is called sterilisation, and the IOUs are called open market operation (OMO) bills.

By end-2025, the Bank had ~$9 billion of these bills outstanding at the closing rate, nearly triple the $2.22 billion outstanding a year earlier.

Step 4: Paying Interest on Its Own Borrowing

Those OMO bills carry interest at or near the monetary policy rate, which ranged from 27 per cent to 21.5 per cent through most of 2025. The Bank paid $1.34 billion in interest to commercial banks for the privilege of borrowing back the cedis it had itself created. That rate has come down significantly but there is no guarantee that it will stay down in the medium-term.

Step 5: The Loss Compounds

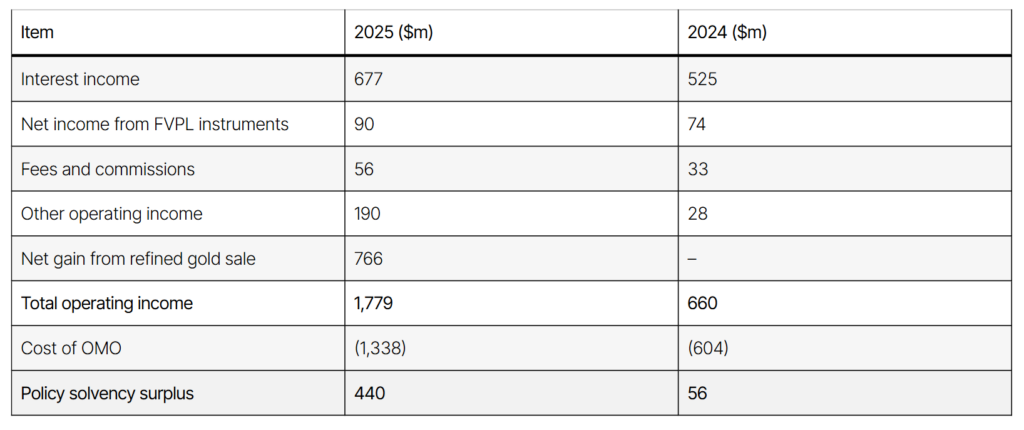

The Bank’s income from all sources – interest on its securities portfolio, fees, and foreign exchange trading, for instance – totalled roughly $1.01 billion in 2025 (excluding the one-off sale of a large part of Ghana’s gold reserves). Its sterilisation costs alone were $1.34 billion. Add operating expenses of $507 million, gold programme losses of $724 million, and other charges, and total operating expenses reached $3.03 billion against total operating income of $1.78 billion. The gap, the annual loss, was $1.25 billion.

That loss worsens an equity position that was already deeply negative. Every year that the cycle repeats the hole will grows deeper.

| In Plain Language The Bank of Ghana is running a three-step operation: (1) print cedis to buy gold, (2) sell the gold for dollars to build reserves, (3) borrow the printed cedis back at high interest to prevent inflation. The operation achieves its strategic goal – record reserves (which contributes to a strong Cedi) + lower inflation – but at a financial cost that exceeds the Bank’s income. |

Policy Solvency: Is the Bank Earning Enough to Do Its Job?

The Bank of Ghana is keen on “policy solvency”: the measure of whether its operating income covers the cost of its main objectives. Remember that the BoG is not like commercial banks. It doesn’t intend to make profits for its shareholders. It only needs to have the resources to implement monetary policy like preventing inflation and Cedi depreciation from getting out of hand.

For 2025, the BoG reported a policy solvency surplus of $440 million. We break down the details below.

Look carefully and you would see that not much changed in its core operations to account for the large jump in income.

Strip out the $766 million one-off gain from selling half the country’s gold reserves, and the Bank posted a policy solvency DEFICIT of roughly $326 million.

The Core recurring income – such as interest, fees, and trading gains – fell materially short of the cost of squeezing cedis out of the system to keep the exchange rate stable, and by implication inflation in check. Policy solvency was achieved only because the Bank liquidated approximately half its gold holdings in a non-repeatable transaction.

Questionable Items Within “Other Operating Income”

The “other operating income” line, which is the only other item that differs materially from 2024, raises all manner of issues. It jumped from ~$28 million in 2024 to ~$190 million in 2025 – a roughly sixfold increase. The financial statements reveal that ~$172 million of this amount was a reimbursement from the Ministry of Finance for “fees and charges incurred in connection with Ghana’s Special Drawing Rights allocation from the IMF.”

It is all sorts of eyebrow raising. The Bank’s own accounts show that its total interest cost on IMF and SDR allocations was $35.6 million in 2025 (Note 11 of the financial statements: 444.8 million GHS). If the actual SDR-related expense was $35.6 million, on what basis did the Ministry reimburse $172 million – nearly five times the stated cost?

The IMF SDR allocations were given to countries as COVID-19 was raging. Normally functioning economies normally don’t touch their SDRs. But Ghana was anything but normal in the 2021 – 2023 timeframe. The records show that Ghana blew through its SDRs and hasn’t bothered to rebuild the holdings, thereby incurring interest expense of $172 million in 2025 on a ~$1 billion IMF SDR allocation. That’s over 17% of the amount.

That figure makes no sense because IMF interest rates for SDR allocations range from zero (if a country doesn’t spend the allocation) to between 3% to 4% in relevant periods. The amount indicated in the financial statements as a refund from the central government to the BoG for handling the interest payments on behalf of Ghana simply doesn’t add up. It is way more than justified by that declared objective alone.

The BoG’s financial statements describe this as reimbursement under “an established cost-sharing arrangement,” but provide no further detail on the calculation methodology or on what cumulative costs are being recovered. If this payment includes arrears from prior years, that context is absent from the notes. BoG seemed to be using accounting gymnastics to raise its income to understate its policy solvency deficit (i.e. that it is not making enough money to cover its core functions.)

Unsettled Gold Receivables

BoG’s “other assets” also jumped from $771 million in 2024 to $2.51 billion at closing rates in 2025. The financial statements do not provide a line-by-line breakdown adequate to explain this surge, but contemporaneous reporting indicates that a substantial portion reflects unsettled dollar proceeds from the Gold for Reserves programme. In that scheme, commercial banks that received gold or gold-linked foreign exchange allocations and had not completed settlement by year-end would have created receivables for the BoG.

However, if approximately $1.2 billion in receivables remain outstanding from programme counterparties, then this raises questions about both counterparty risk within the Domestic Gold Purchasing Program (DGPP) channel and whether the Bank’s reported reserve position includes claims that are not yet liquid.

“Losses” definitely matter

Because the Bank of Ghana creates the currency (Ghana Cedi) in which its obligations are denominated, it does not suffer from losses like a normal commercial bank.

A central bank can and some do operate as a going concern with negative equity. The Czech National Bank ran negative equity for 17 consecutive years after its exchange rate intervention programme generated large foreign-exchange losses. Chile, Israel, Mexico, and Slovakia have all experienced periods of negative capital while conducting effective monetary policy. The Reserve Bank of Australia reported negative equity of A$12.4 billion in 2023 from Quantitative Easing – related bond losses without any disruption to its operations.

But – and this is a very critical qualifier – the fact that a central bank can survive negative equity does not mean it can do so cost-free, or indefinitely, or in any institutional context.

Five ways the BoG’s negative equity situation can affect Ghana badly

1. “Sterilisation” can become a treadmill. Each year of losses means the Bank spent more cedis than it collected. Those extra cedis entered the economy. To prevent inflation, the Bank must sterilise them. It must issue more OMO bills, at more interest cost, generating more losses, and requiring more sterilisation. An effective compounding cycle. At GH¢93.6 billion (~$8.5 billion) in outstanding OMO liabilities and a policy rate in the region of 15 per cent, the annual interest bill alone hovers around $1.12 billion. If the gold programme continues injecting liquidity and the OMO stock keeps growing, the interest bill grows with it – even if the rate falls – because the base is expanding faster than the rate is contracting.

2. Passive money creation. A central bank that spends more than it earns is creating money as a byproduct of its own cost structure. Each dollar of operating loss is a dollar of new cedis that entered the economy without a corresponding withdrawal. In 2025, the Bank’s loss of $1.25 billion represented incremental money creation equivalent to roughly 1 per cent of GDP. We are talking about a structural inflationary impulse that the Bank must then sterilise at further cost. If care is not taken, a dangerous spiral can develop.

3. Negative carry on the portfolio. The Bank borrows short at Ghanaian rates (15 – 27 per cent) and earns returns on its assets at a blend of restructured domestic coupons (suppressed by the DDEP) and international rates (4 – 5 per cent). The result is a mismatch embedded deep in the structure of the Ghanaian economy. As long as Ghana’s risk premium keeps domestic rates well above global rates, the Bank’s portfolio will bleed. No efficiency measure or cost-cutting programme can fix a problem structurally rooted in the country’s term structure.

4. Seigniorage is shrinking. The theoretical defence of central bank losses rests heavily on “seigniorage” (the profit from issuing non-interest-bearing banknotes). As Ghana’s economy becomes more digital (for example: mobile money transactions begin to dwarf physical cash), the share of transactions settled in banknotes will decline. Each transaction that shifts from cash to mobile money reduces the Bank’s seigniorage base, and quietly erodes the income stream that supposedly makes losses irrelevant.

5. The consolidated fiscal position weakens. The central bank and the government are both part of the public sector. The Bank’s annual losses are “quasi-fiscal” deficits. Which is a fancy way of saying that public expenditure that does not appear in the government budget is nonetheless a liability of the government because the central government remains the backstop.

The IMF program targets a government primary surplus of 1.5 per cent of GDP. But if the Bank is simultaneously running quasi-fiscal losses of 1 per cent of GDP, the consolidated public sector position is weaker than the headline fiscal numbers suggest. These shadows can’t be ignored forever.

Recapitalisation: Can the Government Fill a $9 Billion Hole?

The BoG and the Ministry of Finance signed a Memorandum of Understanding (MOU) on 6 January 2025 committing the government to a phased recapitalisation of the BoG over 2026 – 2032. The Bank of Ghana Act was amended (Act 1158) to raise minimum authorised capital from $1 million to $100 million (using USD 1 equals GHS 10 here) and to create a formal framework requiring the government to inject capital within 90 days of the BoG’s Board request.

In the current circumstances, the math looks brutal. Restoring equity from negative ~$9 billion billion to the new statutory minimum of positive $96 million requires approximately $9.1 billion. Spread over six years, that is roughly $1.5 billion annually. An amount equivalent to roughly 8 per cent of the government’s total annual revenue, or about 1.2 per cent of GDP per year.

Is this realistic? Consider the competing demands on the same fiscal envelope:

Fiscal consolidation. The IMF programme requires a primary surplus of 1.5 per cent of GDP. In 2024, the government missed this target by 3.8 percentage points, largely because ministries accumulated GH¢68.8 billion ($4.8 billion) in commitments outside the GIFMIS system. We now know the link to predominantly election-related infrastructure spending. The 2024 audit disqualified 12.5 per cent of these payables for procedural irregularities. Any recapitalisation that adds to public debt works against the government’s embraced IMF’s debt reduction targets, and particularly the lowering of public debt to 47% of GDP by 2030.

Bank recapitalisation. The government is simultaneously recapitalising state-owned commercial banks through the Ghana Financial Stability Fund, which has already disbursed GH¢5.2 billion (~$365 million) in bonds.

Energy sector arrears. Legacy and accumulating debts to independent power producers and fuel suppliers run into billions of dollars over the medium-term. A new fuel levy was introduced in 2025, but its yield covers only a fraction of the annual shortfall.

Infrastructure and social spending. The new administration has committed to expanded social protection, teacher training, and health infrastructure. Plus the Big Push. Each of these is politically non-negotiable.

There are hints that the government intends to handle the recapitalisation by issuing non-tradeable bonds. Such bonds will merely address the equity optic without contributing to operational profitability. The BoG would still needs to earn enough from other sources to cover its sterilisation costs, and the government would still bear the fiscal cost of a larger debt stock.

Fundamental tension: every cedi of recapitalisation bonds adds to the very public debt that the IMF programme is designed to reduce, leading to a very tall order.

GANRAP: The Gold Programme’s Risks Going Forward

The Domestic Gold Purchase Programme (DGPP) has been rebranded as the Ghana Accelerated National Reserve Accumulation Programme (GANRAP). Until the BoG can crack an effective private sector solution, it will continue to purchase domestically produced gold using mostly newly created cedis, convert into monetary gold or sell for dollars, and sterilise the resulting liquidity.

Whilst the DGPP has driven reserves accumulation, the financial cost has been substantial and is structurally embedded in the programme design.

Four structural risks attend GANRAP’s continued operation:

Rate gap. The Bank buys doré at market prices but records it at official rates. The spread between the two – reflecting refining losses, assay fees, GoldBod agent commissions, and offtake discounts – constitutes a permanent operating drain. The Bank has indicated that unit costs are being reduced under GANRAP, but has not published the revised fee & cost schedule.

Sterilisation arithmetic. Each dollar of gold purchased domestically injects approximately GH¢12.50 into the economy (at 2025 average rates). Sterilising that amount at a 15 per cent rate costs the Bank GH¢1.88 per year – or $0.15 per dollar of reserves acquired. Over a two-year holding period before the gold is refined and banked, the sterilisation cost alone consumes 30 per cent of the dollar value of the reserve gain. Central banks that acquire reserves by purchasing dollars with existing cedi holdings, or by receiving IMF disbursements, incur a fraction of this cost.

GoldBod counterparty exposure. The Bank’s specific exposure to GoldBod, the intermediary for artisanal and small-scale gold purchases, is not separately disclosed in the financial statements. The IMF’s 5th ECF Review noted that losses from artisanal and small-scale gold transactions had reached $214 million. We now know that the overall exposure was more than 4x that amount. The Gold-for-Oil programme (which used gold sales to finance petroleum imports) was discontinued in March 2025 after cumulative losses, but the G4R programme continues under a new label with the same intermediation structure.

Diminishing marginal returns. Ghana’s reserves at $13.8 billion provide 5.7 months of import cover. Each additional dollar of reserves provides incrementally less insurance value. The jump from 1 month to 3 months of cover is transformative; from 5 to 6 months, the marginal benefit is modest while the sterilisation cost remains constant. Continuing to accumulate at 2025 pace imposes annual costs exceeding $1 billion for diminishing strategic gain. And now there is talk of jacking up coverage to 15 months based on large monthly purchases of gold. A situation that will jack up gold channel – sterilisation costs, lead to much higher opportunity cost of resources tied up in reserves earning minimal interest, and all for very modest insurance benefits.

Alternative Approaches with Lower Costs

The Bank of Ghana’s method of reserve accumulation – domestic gold purchase financed by money creation and sterilised at domestic interest rates – is among the most expensive possible approaches. Several alternatives would deliver similar or superior results at lower financial cost:

1. Mandate gold royalty payments in-kind rather than in cash. Large-scale mining companies currently pay royalties in cedis. If a more significant portion were payable in refined gold delivered directly to the Bank’s reserve account, the Bank would acquire gold without creating any domestic liquidity. No sterilisation cost because the gold arrives already refined. Drawback: requires legislative amendment and renegotiation of mining agreements. Companies would resist because it removes their flexibility to time royalty payments. Still an idea worth exploring further.

3. Channel gold purchases through a fiscal agent rather than the central bank. If the Ministry of Finance (or a sovereign wealth vehicle) purchased gold using existing budgetary resources and transferred it to the Bank, the liquidity injection would come from fiscal spending already accounted for in the budget – rather than from new money creation. The Bank would receive gold without printing cedis, eliminating the sterilisation cost entirely. Drawback: requires fiscal space that the government does not currently have, and creates a different form of fiscal-monetary entanglement.

4. Slow the pace of accumulation. With reserves at 5.7 months of import cover, Ghana has already exceeded the standard adequacy threshold. Reducing the pace of domestic gold purchases by 50 per cent would halve the sterilisation cost while maintaining reserves above comfortable levels. Drawback: politically difficult. The gold programme is popular, enriches domestic capitalists, and aligns with resource nationalism sentiments. GoldBod, mining communities, and aggregators are all powerful constituencies.

5. Restructure the entire gold channel creatively. We have recently described a “Trust-Chain” model that could shift GoldBod from state trader to regulator of a transparent, competitive gold network. Private or semi-private financiers fund aggregators, multiple buyers compete for gold, offtake is auctioned broadly, and risks like price, purity, FX, and logistics are explicitly allocated rather than dumped on BoG. In the proposed model, real-time traceability, published benchmarks, audits, and risk-sharing preserve reserve-building benefits while reducing subsidies, opacity, and public balance-sheet losses.

The political economy barriers to all these alternatives are formidable. The DGPP/GANRAP has created a domestic ecosystem of aggregators, agents, transporters, and small-scale miners who depend on continued central bank purchases. GoldBod itself is a relatively new institution with institutional momentum. Slowing or restructuring the programme would generate concentrated losses among these groups while distributing diffuse gains (lower inflation risk, and reduced central bank losses) across the general population.

If you know your katanomics theory well you also know that this is exactly the political dynamic that makes reform difficult in any democracy. Simply because there simply isn’t a critical policy audience to constitute a counterweight to the political jobbers and vested interests.

So long as the Cedi remains stable and inflation stays down, apathy about the situation shall dominate.

Should citizens care?

To wrap up, these are the key issues to keep track of.

Inflation risk. The sterilisation treadmill creates a latent inflation reservoir. The GH¢93.6 billion in OMO bills will eventually mature. If the Bank cannot roll them over – because banks demand higher yields, or because the stock has grown too large relative to the banking system’s appetite – the cedis flood back into the economy. In 2025, the OMO stock was equivalent to roughly 34 per cent of broad money (M2+). An uncontrolled unwinding of even a quarter of this stock would release enough liquidity to reignite inflation sharply.

Higher borrowing costs. Commercial banks earning 15 – 25 per cent risk-free on OMO bills (as the policy rate rebounds) have little incentive to lend to businesses or households at comparable rates. Why take credit risk on a small enterprise when the central bank offers guaranteed returns? The OMO book crowds out private credit. If the OMO stock remains bloated, lending rates to businesses and households will remain elevated.

Forgone government spending. Every cedi the government eventually transfers to recapitalise the Bank is a cedi not spent on schools, hospitals, roads, or social protection. If the recapitalisation MOU is honoured, $1.3 billion per year – roughly equivalent to Ghana’s entire 2024 capital expenditure on health – will flow from the Treasury to the Bank’s balance sheet for seven years. If the MOU is not honoured, the Bank’s negative equity persists, and the risks described above intensify.

Currency vulnerability. The cedi appreciated 41 per cent against the dollar in 2025 – a remarkable performance driven by strong reserves, high real interest rates, and improved investor confidence. But this appreciation was partly sustained by the very OMO operations that are financially unsustainable for the Bank. If the Bank is forced to reduce sterilisation (because the cost is too high), excess cedis will chase dollars, reversing the appreciation. A 20 per cent depreciation from current levels would erase the purchasing power gains that Ghanaian households experienced in 2025 and push imported food and fuel prices higher.

Conclusion: yes, citizens should care

The Bank of Ghana’s negative equity, taken in isolation, is not the catastrophe that partisan commentary suggests. Central banks are not commercial banks. They do not face insolvency in the conventional sense. Their mandate is price stability and financial system soundness, and the Bank has delivered measurably on both in 2025: inflation fell to 5.4 per cent (within the target band for the first time since 2021), reserves reached historic highs, the banking sector returned to profitability, and the cedi’s appreciation was the strongest among emerging market currencies.

What should worry us is the sustainability of the operating model that produced these results. The Bank ran a $1.25 billion loss to achieve them. It achieved policy solvency only by liquidating half its gold reserves – a one-time manoeuvre. Core operating income fell $326 million short of sterilisation costs. The OMO liability stock tripled in a year. The recapitalisation plan depends on a government that has never sustained seven consecutive years of fiscal discipline. And several items in the financial statements – the SDR reimbursement, the unsettled G4R receivables, and the opacity of GoldBod exposures – suggest that the reported numbers may present a more favourable picture than the underlying reality warrants.

The gold programme has been clearly impactful regarding reserves. But as we have seen, it can be greatly improved.

Ghana’s economy has absorbed extraordinary shocks since 2022 – sovereign default, debt restructuring, currency collapse, inflation above 50 per cent etc. The Bank of Ghana deserves some credit for the signs of recovery. But the institution’s balance sheet is carrying the accumulated cost of stabilisation in a way that constrains its future flexibility.

If the next shock arrives before the balance sheet is repaired, the Bank will face it with less ammunition, less credibility, and less room to manoeuvre than it had in 2022.

No one can say that this is not something citizens should worry about.

Credit: brightsimons,com

The author, Bright Simons, is a Ghanaian technologist, social innovator, entrepreneur, writer, social and political commentator. He is the vice-president, in charge of research at IMANI Centre for Policy and Education. He is also the founder and president of mPedigree.

Commentary

Reflections on Ghana And the Future it Deserves | By Simone Giger, Swiss Ambassador to Ghana

As her diplomatic tenure in West Africa draws to a close, Swiss Ambassador Simone Giger pens a reflective and heartfelt tribute to Ghana’s enduring national character. Having traveled extensively across the country—from Paga to Keta and Wa to Goaso—she offers an intimate, human-centered assessment of a nation defined by its resilient democratic culture, youthful ambition, and an infectious “vibe” that fosters cohesion. In this candid farewell, Ambassador Giger explores the complex challenges threatening Ghana’s ecological treasures and argues that sustained institutional reform, rather than outside invention, is the key to unlocking the prosperous future the country so clearly deserves.

Travelling through northern Ghana, this author once stopped in a small community after a long journey. Despite the day’s heat and the demands of daily life, residents welcomed visitors with warm smiles, easy laughter and an eagerness to share stories about their hopes for the future.

It was a simple encounter, yet it captured something profoundly Ghanaian: an enduring optimism that persists even in difficult circumstances.

In diplomacy, countries are often assessed through official meetings, economic indicators and policy documents. Yet to truly understand a nation, one must travel through it, listen to its people, appreciate its strengths, observe its contradictions and understand the aspirations that shape everyday life.

As the end of a diplomatic assignment in Ghana approaches, this author finds reason to reflect deeply on a country that has left a lasting impression, not only professionally but personally.

Over the past four years, extensive travels across Ghana—from Paga to Keta, Damongo to Donkokrom, and Wa to Goaso—have revealed a country of extraordinary diversity, complexity, creativity and resilience.

Every journey has unveiled a different dimension of Ghana. Yet one common thread consistently emerges: a nation brimming with potential.

There is something profoundly remarkable about Ghana and its national character, what many Ghanaians simply describe as the country’s “vibe”.

It is evident in the warmth extended to strangers, the humour with which difficulties are confronted and the optimism that endures even during periods of uncertainty.

Even in challenging moments, there is often a joke, a proverb or a story that helps place events in perspective.

In this author’s view, that national character has become one of the essential ingredients behind Ghana’s democratic success.

At a time when democratic systems around the world are facing increasing pressure, polarisation and distrust, Ghana continues to distinguish itself through its commitment to dialogue, constitutional order and peaceful coexistence.

Democracy here is not perfect. No democracy truly is, including Switzerland’s.

What matters is that it remains alive, active and deeply valued by citizens.

Over the years, Ghana has established itself as an important democratic reference point in West Africa.

The country has repeatedly demonstrated that political competition can coexist with stability, that transfers of power can occur peacefully and that national debates can take place within institutional frameworks rather than outside them.

Such achievements should never be taken for granted.

Democracy is not sustained by elections alone.

It requires strong institutions, active citizens, credible public discourse and a continuous willingness to negotiate consensus across political, ethnic, religious and generational lines.

One can observe that Ghana’s diversity presents both opportunities and challenges. Yet this author has often admired the manner in which the country continues to navigate these varied interests while preserving national cohesion.

In many respects, this is where Ghana’s democratic future becomes particularly important.

The country possesses extraordinary human capital.

Wherever this author travelled, young people displayed ambition, intelligence, creativity and determination.

Ghana’s greatest resource is not found beneath the ground.

It resides in its people, their ideas and their aspirations.

Ideas and aspirations, however, require systems that function effectively if they are to translate into meaningful and productive outcomes.

When institutions are transparent, responsive, accountable and trusted, they unlock innovation, investment and opportunity.

When they are weak or inconsistent, they risk frustrating the very energy capable of propelling a nation forward.

This is why governance reforms remain so important to Ghana’s long-term trajectory.

One development that particularly impressed this author during the diplomatic assignment has been Ghana’s constitutional review process.

What stands out is not only the process itself, but also the spirit behind it – a willingness to reflect critically on how democratic governance can evolve to meet contemporary realities and future expectations.

This demonstrates political maturity.

Constitutions should never be viewed as static documents frozen in time.

Strong democracies periodically examine whether their systems remain responsive, inclusive and effective.

Ghana’s consultative approach reflects a country seeking not merely to preserve democracy, but to improve it.

Switzerland is proud to support these home-grown efforts and remains committed to supporting the constitutional reform process until its hoped-for successful conclusion.

History demonstrates that democratic stability does not emerge automatically.

It requires deliberate investment in participation, inclusion and dialogue.

Swiss democracy itself evolved gradually through compromise, negotiation and the understanding that national cohesion is strengthened when citizens feel ownership over public decisions.

One can observe important similarities between Ghana and Switzerland.

Both countries are diverse societies that have chosen coexistence over division.

Both understand that stability is strongest when different voices are heard and accommodated.

Both appreciate the importance of consensus-building in national life.

This shared philosophy has shaped bilateral cooperation over many decades.

Today, the partnership continues to evolve in both breadth and depth.

Switzerland currently supports initiatives focused on democratic governance, parliamentary cooperation, decentralisation, peace and security, cultural exchange, environmental integrity, climate adaptation and economic development.

Switzerland and Ghana may differ in geography, history and scale, yet both countries share a belief in dialogue and cooperation as foundations for national progress.

Despite Ghana’s bright prospects, one cannot ignore the challenges confronting the country.

No nation can fully realise its potential without confronting difficult issues directly.

During the years spent in Ghana, citizens from various walks of life spoke openly about concerns surrounding institutional effectiveness, economic opportunity, environmental degradation and governance accountability.

Such conversations reflected not pessimism, but a desire to see the country fulfil its promise.

Particularly concerning is the destruction caused by illegal mining activities.

Ghana’s rivers, forests and landscapes are among its greatest treasures.

Environmental degradation is not merely an ecological issue.

It is fundamentally a matter of intergenerational responsibility.

Future prosperity depends on preserving the natural foundation upon which communities, livelihoods and national identity are built.

Yet despite these challenges, this author remains deeply optimistic about Ghana’s future.

That optimism stems not from idealism but from observation.

The future of democracy globally will not be shaped only by geopolitical actors or large states.

Medium-sized countries such as Switzerland and Ghana also have important roles to play.

They can demonstrate that democratic resilience, peaceful coexistence and institutional reform remain both possible and necessary.

As this diplomatic assignment draws to a close, there is profound gratitude for the opportunity to have lived and worked in Ghana.

Over the years, this author has come to admire the country not only for its democratic achievements, but also for its humanity – its warmth, creativity, humour and enduring sense of possibility.

The task ahead is not to invent Ghana’s future.

Rather, it is to create the institutional conditions necessary for that future to emerge fully.

From all that has been observed across the country, there is every reason to believe that Ghana can achieve precisely that.

The author, Simone Giger, is the Swiss Ambassador to Ghana, Togo and Benin

This article by Joseph McCarthy, an analyst and researcher focusing on governance, security, and political transitions in the Sahel, argues that modern influence in Africa often spreads not through propaganda but through credible African voices that carry narratives aligned with the interests of external powers. Read the full article below.

Authentic Voices, Foreign Narratives and the Fortune Madondo Case

How Russian narratives are travelling through authentic African voices, and what the Fortune Madondo case reveals about it

By Joseph McCarthy

For years, the word disinformation conjured a familiar picture: troll farms, fake accounts and automated bots flooding the internet with crude propaganda. Those methods still exist, but influence operations have matured. The most effective messenger today is rarely an anonymous account. It is a real person, with a real name, a credible public profile and convictions he appears to hold sincerely.

The case of Fortune Madondo illustrates the shift. He is no online provocateur hiding behind a pseudonym; he is a Zimbabwean teacher and the founder of a youth organisation, with a documented life in his community. He writes under his own name, identified in his byline only as an “African Teacher,” with no institution given, and his views seem consistent with his stated beliefs. What matters is less who he is than what he carries. Across more than fifty articles in twelve months, most of them on Pan-African platforms, the line never wavers: praise for the military juntas of the Sahel, attacks on Western governments and on AFRICOM, condemnation of France’s role in Africa, and the celebration of resource sovereignty against foreign plunder. Whether by design or by conviction, these themes closely align with the narratives Moscow has sought to amplify across the continent.

That alignment, not the man, is the point. Influence no longer requires recruitment, payment or instruction. A foreign power’s objectives can be served just as well by people who believe every word they write, because the force of the message lies in its local authenticity. A reader will trust an African voice discussing African problems far sooner than a communiqué from Moscow. So the useful question is not whether Fortune Madondo is a Russian agent; there is no public evidence that he is. The question is who benefits when local voices, sincere or not, repeatedly reinforce narratives that happen to serve a foreign strategy.

Consider how this interacts with Pan-Africanism. Russia has spent years presenting itself as a champion of African sovereignty and an enemy of colonialism, language that resonates because it draws on real historical wounds. Madondo’s writing sits comfortably within that tradition, and many African intellectuals share his instincts. Yet the scrutiny runs in only one direction. The West is relentlessly interrogated; Moscow, despite its expanding military, mining, and political footprint, is almost never asked the same questions. If Pan-Africanism is the defence of African sovereignty against all external control, the principle must apply evenly. When French deployments are called neo-colonial, Russian military contractors deserve the same examination; when Western extraction is condemned, so should Russian mining concessions. When he co-signed an appeal in late 2024 demanding both that Russian troops leave Ukraine and that French troops leave Africa, the false symmetry itself did Moscow’s work. A Pan-Africanism that suspects only one power risks sliding from a doctrine of independence into an instrument of another’s ambition.

The Madondo question also points to a place: Ghana. Over the past two years, the country has drawn growing attention from foreign actors keen to enter its media space, and the reason is structural. Ghana is one of Africa’s most respected democracies and a heavyweight in anglophone media; what is published in Accra travels across West Africa and beyond. In December 2025, Ghanaian journalists attended a SputnikPro seminar co-organised by the Russian Embassy and the Ghana-Russia Centre, led by Vasily Pushkov of Rossiya Segodnya, the state group behind the Sputnik news agency. Other moves followed, among them a cooperation agreement with Ghana’s main journalism university and the opening of a Russian cultural centre. None of this is illegal. But influence secured in Ghana enjoys a multiplier effect that few other markets offer.

The mechanism is quieter than propaganda and more durable. People do not trust propaganda; they trust outlets they already consider credible. A publication earns that trust through genuine local reporting, and the reader then assumes that everything on the page has cleared the same editorial bar. That is where credibility is transferred: from the newsroom’s real work to syndicated columns, opinion pieces and, on some platforms, verbatim Russian state material set at the same level as a story on local agriculture. Repetition completes the effect. Ten near-identical articles across ten outlets read as an independent consensus; the reader concludes that everyone is saying this, when in truth, the same viewpoint is simply circling back. Influence here comes not from proving a claim, but from normalising it.

The significance of the Madondo case, then, is not the unmasking of an operative; the evidence does not support that, and the chase would miss the point. It is the growing difficulty of telling sincere conviction apart from narratives engineered to serve someone else’s strategy, in an environment where influence travels through authentic voices, trusted platforms and ideas that genuinely resonate. The defence is not a hunt for enemies but the slower work of critical thinking, editorial transparency and media literacy. The question is no longer simply who is speaking. It is whose interests are served when the same narrative is amplified, again and again, across the continent.

Joseph McCarthy is an analyst and researcher focusing on governance, security, and political transitions in the Sahel. He writes on geopolitics, development, and African diplomacy. Email: joecarthy30@gmail.com

Ghana has inked a £215 million ( $287. 5 million) deal with the United Kingdom, anchored by a £101 million ($135.05 million) floating dock in Takoradi.

If successful, it will become the Gulf of Guinea’s first modern, commercially operated ship repair facility.

Here is what is at stake.

1. The Gulf of Guinea Loses Millions While Ships Sail Elsewhere for Repairs

The Gulf of Guinea is one of Africa’s busiest shipping corridors, crowded with oil tankers, cargo vessels, and offshore support ships. Yet almost all major repairs happen outside the region, often in Namibia, Spain, or beyond. Every vessel that bypasses West Africa carries away not just steel but also jobs, technical knowledge, and national revenue. The region pays the repair bill elsewhere and receives none of the associated economic ripple effects.

2. A Floating Dock Is Only the Beginning – The Real Prize Is a Maritime Services Cluster

The dock itself is just hardware. The true opportunity lies in building a complete ecosystem around it: logistics, steel fabrication, waste management, security, crew training, catering, and port-side supply chains. Without these supporting industries, the dock becomes an isolated asset rather than an engine of local employment.

3. Ghana Already Has Indigenous Firms Ready to Scale

Homegrown players such as Rigworld have proven capabilities in marine and industrial services. The pivotal question is whether this project allows those firms to grow or whether foreign operators will absorb the most valuable contracts. Local-content policies will determine the answer.

4. Success Depends on Transparent, Proactive Government Measures

Infrastructure alone guarantees nothing. Authorities must publish tender opportunities clearly and early, establish a centralized supplier portal, offer certification support to local businesses, and ensure that Ghanaian small and medium enterprises can access affordable working capital. Without deliberate rules, international firms may capture the entire supply chain while domestic companies watch from the shore.

5. If Ghana Succeeds, Takoradi Becomes a Blueprint for African Value Retention

Should Ghana get this right, the floating dock could become a template for how African economies retain more value from their own geographic advantages. If it fails, the region will simply have acquired another expensive piece of imported equipment with little local benefit. The Gulf of Guinea offers no shortage of ships. Whether Ghanaian businesses—not just foreign firms—will profit from them remains the only question that truly matters.

The Hidden Real Estate Factors Behind a Successful Relocation

Ghana Vows to Avoid ‘Narco-State’ Label as it Arrests Lead Suspect in $296M Australia Meth Case

Accra Set to Host Pan African AI & Innovation Summit 2026

-

Ghana News1 day ago

Ghana News1 day agoThomas Partey Declares Readiness for England Showdown, Electricity and Water Tariffs Increase, and Other Big Stories in Ghana Today

-

Arts and GH Heritage1 day ago

Arts and GH Heritage1 day agoGhana to Build Modern Museum as Permanent Home for 2,000 Looted Artefacts Returned from Europe

-

Ghana News1 day ago

Ghana News1 day agoAfricans and Diaspora to Exclusively Lead Design of Ghana’s New Slavery Museum

-

Ghana News1 day ago

Ghana News1 day agoGhana’s top 10 newspaper front-page headlines: floods, shooting probe, Rawlings tribute, and World Cup clash dominate

-

Reels & Social Media Highlights1 day ago

Reels & Social Media Highlights1 day ago#BlackStars and Beyond: The Unmissable Trends Dominating Ghana’s Social Space

-

Festivals & Events13 hours ago

Festivals & Events13 hours agoInside DASA 2026: The Summit Bringing Blockchain Innovation to the Heart of Ghana

-

Health & Wellness2 days ago

Health & Wellness2 days agoThe Postpartum Nutrition Secret More New Mothers Should Know

-

Taste GH12 hours ago

Taste GH12 hours agoMore Than a Meal: Why Cooking in Ghana Is Considered an Art